Every Little Thing You Ought To Know About Residence Mortgages

Authored by- please click the next siteBefore getting a mortgage, you must first take many steps. The main thing you have to do first is to learn everything you can about getting a loan that's secured. That process begins by reading below to learn all the tips and advice that will aid you through this process.

You probably need a down payment. In years past, buyers could obtain financing; however, most do require a down payment now. You should know what the down payment is before applying.

If you are considering quitting your job or accepting employment with a different company, delay the change until after the mortgage process has closed. Your mortgage loan has been approved based on the information originally submitted in your application. Any alteration can force a delay in closing or may even force your lender to overturn the decision to approve your loan.

Once you have chosen the right loan for your needs and begun the application process, make sure to get all of the required paperwork in quickly. Ask for deadlines in writing from you lender and submit your financial information on time. Not submitting your paperwork on time may mean the loss of a good interest rate.

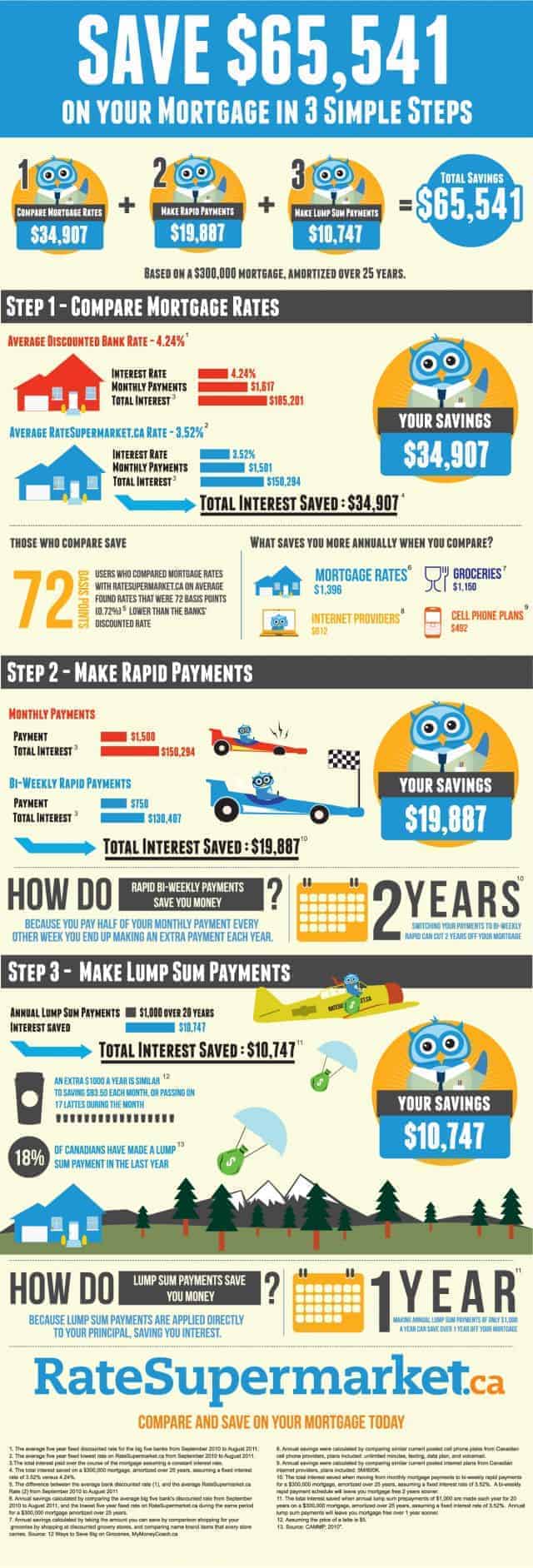

Get quotes from many refinancing sources, before signing on the dotted line for a new mortgage. While rates are generally consistent, lenders are often open to negotiations, and you can get a better deal by going with one over another. Shop around and tell each of them what your best offer is, as one may top them all to get your business.

If you are a veteran of the U.S. Armed Forces, you may qualify for a VA morgtage loan. These loans are available to qualified veterens. The advantage of these loans is an easier approval process and a lower than average interest rate. The application process for these loans is not often complicated.

When you decide to apply for a mortgage, make sure you shop around. Before deciding on the best option for you, get estimates from three different mortgage brokers and banks. Although, interest rates are important, there are other things you should consider also such as closing costs, points and types of loans.

Don't apply for new credit and don't cancel existing credit cards in the six months before applying for a mortgage loan. Mortgage brokers are looking for consistency. Any time you apply for credit, it goes on your credit report. Avoid charging a large amount during that time and make every payment on time.

Find out if the loan you are applying for is a fixed rate or adjustable rate loan. Generally adjustable rate loans offer lower interest rates; however, the interest rate can increase over time. With an adjustable rate loan, your interest rate can increase yearly; thus costing you more money in the long run.

A good credit score is essential if you want to finance a home. If your score is below 600 you have some work to do before you can hope to purchase a home. Begin by getting a copy of your credit record and verifying that all the information on it is correct.

Before looking to buy a house, make sure you get pre-approved for a mortgage. Getting pre-approved lets you know how much you can spend on a property before you start bidding. It also prevents you from falling in love with a property you can't afford. Also, many times seller will consider buyers with pre-approval letters more seriously than those without it.

Make sure that you have a good amount of savings before you get yourself into a home mortgage contract. There are not certainties when it comes to the economy or job stability. To protect yourself you want to have enough money saved to make your payments for many months in case the worst does occur.

Remember that there are always closing costs and a down payment associated with a home mortgage. Closing costs could be about three or four percent of the price of the home you select. Be sure to establish a savings account and fund it well so that you will be able to cover your down payment and closing costs comfortably.

If you have previously been a renter where maintenance was included in the rent, remember to include it in your budget calculations as a homeowner. A good rule of thumb is to dedicate one, two or even three perecent of the home's market value annually towards maintenance. This should be enough to keep the home up over time.

Understand what happens if you stop paying your home mortgage. It's important to get what the ramifications are so that you really know the seriousness of such a big loan as a home mortgage. Not paying can lead to a lower credit score and potentially losing your home! It's a big deal.

Being upfront and honest about your financial situation is crucial when applying for a loan. If why not look here , you may be denied the loan you seek. A lender will not put their trust in you if you can't be bothered to tell the truth.

Think about getting a mortgage where you are able to make payments bi-weekly. This will increase the number of payments you make per year to 26 instead of 12, giving you 2 extra payments. You might even have the payment taken out of your bank account every two weeks.

Think about refinancing your home mortgage so that you are paying more towards the principle each month. The more that you pay on the principle, the less you will pay in the long run. This is the perfect option for you if you now make more money than you had when you signed the original contract.

During the process of obtaining a mortgage loan, submit any requested documents to your mortgage broker or lender as soon as possible. Taking your time to respond to your lender can delay the date of the closing. Delaying the closing date can put you at risk of losing the rate you have locked-in.

The last thing you want to do is to sign the paper for your mortgage and days or months later find out you made a really bad mistake. Instead, you want to be confident that you have made a really good decision. Move forward with the tips that have been provided to you and choose wisely.